The EPC has responded to the Department for Education’s technical proposals for an international student levy. Although this was a technical consultation, we wanted to follow up on our letter to the Skills Minister – Baroness Smith – and her response following our analysis of the financial impact that the International Student Levy will have on Engineering higher education. We chose to respond to question 8 only: Do you think the proposed restrictions to the scope of the levy would have any unintended consequences on the behaviour of students or providers?

The scope of the proposed flat fee levy of £925 (broadly equivalent to a 4.5% fee) per international student per year would have unintended consequences on the behaviour of providers, encouraging course portfolio shifts away from strategically important Engineering courses to those that make a surplus on domestic students.

This is critical for three reasons which, taken together, mean that an international levy risks taxing the supply chain of the Industrial Strategy itself.

- Engineering courses are vital to deliver the skills pipeline for the IS8 sectors and associated regional development. Four of the eight IS8 sectors are explicitly Engineering sectors and the others will all draw heavily on those same skills.

- Real terms falling tuition fee investment for the past 13 years has led the sector to a position where high-quality provision for home Engineering students is loss-making.

- Engineering departments are among those most dependent on international student fee income; one in four Engineering first degree students are from overseas (compared with one in seven across all subjects). International students – and PGT students, in particular – currently provide a crucial cross-subsidy that helps sustain Engineering provision at scale, offsetting losses incurred on UK undergraduate courses.

In order to offset the levy, HE providers will have to either:

- increase international fees, where the market allows (which would be limited), to support the same number of domestic Engineering students;

- increase international student numbers for the same reason, where the market allows (which would, again, be limited);

- reduce domestic student numbers;

- reduce costs which may have an impact on quality of education;

- close Engineering courses.

These options are not all mutually exclusive and none would have a positive effect on the skills pipeline in Engineering. The system-wide effect would undoubtedly be damaging.

Given the 3 reasons cited above, the levy fee will disproportionately target Engineering and, by extension, the income stream currently sustaining IS-8-relevant Engineering provision. It would accelerate domestic decline and weaken the UK’s ability to deliver on its stated ambitions for growth, productivity and technological leadership.

By increasing the cost of recruiting overseas PGT students, in particular, a levy would reduce demand in precisely the segment that is currently keeping high-cost Engineering disciplines viable. The likely consequence would be course closures, reduced capacity, or further retrenchment.

The recent shift in General Engineering enrolments exemplifies why an international student levy would be counterproductive. General Engineering is the most expensive Engineering discipline to deliver[1]. Between 2019 and 2023, UK-domiciled student numbers fell by 7%, largely due to declines in undergraduate recruitment, despite increasing numbers of undergraduate applications to Engineering. At the same time, overseas enrolments increased by around 1,860 students, almost entirely driven by postgraduate students (typically PGT non-EU). Critically, these enrolment trends are system-wide in Engineering, not concentrated in a small number of providers.

This growth in international PGT provision is not accidental. It reflects how universities have responded to long-standing underfunding of high-cost subjects for UK students. Mounting pressures are well rehearsed and have forced the sector to do more with less for over a decade; Engineering learning environments come with high fixed costs which themselves need to remain fairly static to ensure the equipment is maintained and accessible to all students for a high-quality experience. Consequently, Engineering is highly vulnerable to market volatility.

Assuming that providers will, to a greater or lesser extent, pass on the cost of the levy to international students via increased tuition fees means that the burden falls disproportionately on universities that are more price sensitive. EPC analysis of international (undergraduate)fees in different parts of the sector highlights non-uniformity and suggests that less expensive courses are those with lower price elasticity:

- Russell Group universities: £28,762

- Pre-92 universities: £19,509

- Post-92 universities: £14,729

Rudimentary modelling of the impact assessment scenarios in Engineering departments highlights a potential c20% loss in overseas income by 2025/6, with the extent of the threat largely aligning with Vicki Bolliver’s elasticity clusters cited in the consultation. Institutions in the Russell Group account for over 60% of the international fee income to the sector despite accommodating <50% of the international student cohort. Clearly, the introduction of a flat fee impacts those with lower fees more severely as proportionally it is a larger percentage of their international income. So, while Oxford and Imperial, for example, are more likely to be able to mitigate the loss by increasing their fees and remaining attractive and viable, non-Russell group providers – hosting over half of international Engineering students – may not.

Meanwhile, there is no evidence that these courses are lower quality. Engineering has almost universally good employment outcomes across all providers and, unlike many subject areas, it is often a key strength in institutions that aren’t not traditionally at the top of league tables. That’s partly because Engineering has better ties to industry than most courses and Engineering firms are often found away from traditional economic centres like London. We suggest that the very courses in the very universities that will be hardest hit by the levy are the ones most important to IS8 and to regional development goals.

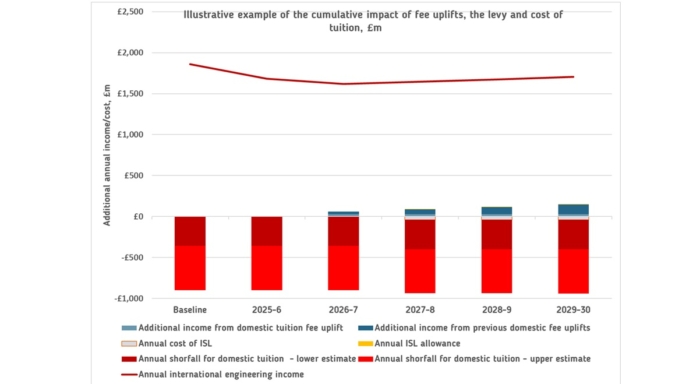

We warmly welcome that the index-linked proposals stabilise domestic undergraduate tuition fees by ensuring that they do not fall further in real terms, but it is important to recognise that this is in the context of an unsustainable baseline arising from the legacy shortfall per domestic Engineering student. (See the graph which demonstrates the shortfall estimates and reduced international engineering income (i.e. the product of the fee uplift minus the international fee income net of government forecast decline in international students).

The EPC estimate this shortfall at an average of £7,591 per student across Engineering (more in General Engineering) in 2023/24 (including adjustment for the high-cost funding uplift for institutions delivering strategically important subjects).

Given the Government’s clear strategic missions, it is all the more important that the international student levy does not undermine Engineering education in real terms. While the inflation-linked tuition fee uplifts are sector-wide, the international levy disproportionately targets IS8 critical sectors; four of which are Engineering while the other four are Engineering related. It is counterproductive to both the Industrial and International Education strategies to target one of the most internationally attractive and strategically important disciplines in this way (not least because historically the UK’s Engineering workforce has relied on international graduates remaining in the Engineering sector just to stop skills shortages from growing, but now the skills demand is set to grow further).

The extent to which the introduction of an international levy would directly weaken the fragile HE Engineering funding model can be explored by considering the reliance on overseas PGT Engineering fees at provider level. We estimate that for half of the 70 English Engineering providers we examined (those with the largest Engineering contingents) overseas student fee income from Engineering exceeded the domestic fee income from Engineering – across providers of all types, including Russell Group, in 2023/4. In over one third of these providers (again, across a range of provider types, and regions), estimated that Engineering fees in 2023/4 represented over 10% of provider fee income[2], with overseas Engineering tuition fees alone contributing over 10% at seven providers. This represents a significant dependency of domestic Engineering education on overseas income.

This means the impact of an international levy would also be systemic, disproportionately harming strategic STEM capacity across the sector rather than targeting excess or low-value provision.

In effect, an international levy risks penalising the very income stream that is compensating for domestic underfunding, accelerating the decline of UK-domiciled participation in Engineering and undermining national skills objectives. Rather than addressing structural funding gaps, the levy would amplify them.

An international levy would clearly be in direct conflict with IS-8 objectives. The forecast reduced demand in the very programmes that support strategic industrial priorities is likely to weaken the financial viability of Engineering departments that serve these sectors. The result would likely be reduced capacity, course closures, or a narrowing of provision, particularly in capital-intensive and laboratory-based fields.

This contradiction is structural, not marginal. The enrolment trends in the General Engineering example we offer are system-wide, meaning the effects of a levy would be felt across the national skills base, not absorbed by a few providers. In practice, the levy would undermine the delivery mechanism for the Industrial Strategy while leaving the underlying problem — insufficient domestic funding for high-cost IS-8 subjects — unresolved.

In the technical design of the scope of this policy, there are a number of possible ways to mitigate these problems:

- Excepting high-cost strategically important subjects from the International Levy proposals.

- Reducing the international levy for strategically important subjects.

- Raising the provider allowance from the 220 proposed for providers who offer strategically important IS8 Engineering subjects or permitting an additional allowance for students in those subjects

- Taking the opportunity of the forthcoming review of the Strategic Priority Grant to counter this effect through a significant uplift for Engineering (and IS-aligned courses) through the SPG.

- Applying any or all of these measures selectively to Engineering PGT courses.

- A combination of any or all of the above.

We would also urge Government to rigorously review the applied policy to assess the market impact it has over time.

[1] Based on TRAC estimated average full teaching cost 2018/9 and 2025/6 for an OfS funded FTE Engineering student for 2018/19 (based on 2015-16 data returns for higher education institutions in England and Northern Ireland, uprated to 2018-19 prices to account for inflation based on UUK uplift4 . Uses HESA cost centre. https://epc.ac.uk/article/epc-petitions-government-ahead-of-the-comprehensive-spending-review/

[2] HESA Finance Combined Table 7.